The Re-Calibration of Bitcoin's Risk-On Profile in the Era of the 2026 U.S.-Iran Peace Accord

Deep dive Bitcoin analysis and looking at how Bitcoin's Risk-On Profile has changed after the US-Iran Peace Accord. What does price performance look like for the rest of 2026?

ANALYSIS

Tayler McCracken

6/16/202618 min read

Executive Summary

The 2026 U.S.-Iran peace accord acts as a critical macroeconomic release valve, neutralizing the energy-driven stagflation threat that previously suffocated global liquidity. By unburdening central banks from hawkish constraints, this agreement creates a structural liquidity catalyst, positioning Bitcoin to outperform as a primary beneficiary of the looming global monetary expansion.

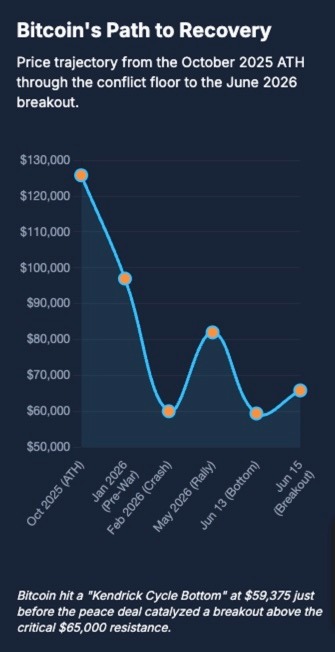

The white smoke rose from a closed-door session in Tehran on Sunday night, June 14, 2026, and by the time the European trading desks blinked open, the trading algorithms had already made up their mind. After 15 grueling hours of radio silence from the Qatari mediators, the announcement of an interim U.S.-Iran peace agreement hit the wires.

The $82 Liquidity Trigger Traditional Analysts Are Misreading

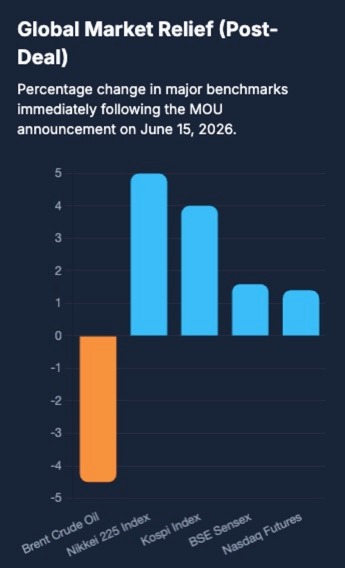

The market reaction was instantaneous, violent, and entirely predictable. Brent crude futures, which had been pricing in a permanent geopolitical risk premium for over three months, fell off a cliff, plummeting 5.2% in a single trading session to settle between $82 and $83 a barrel. The maritime chokeholds were easing, the threat of an imminent broader conflagration was receding, and across the financial landscape, risk models were being systematically rewritten.

Predictably, the knee-jerk reaction from the crypto commentariat was outright panic. As spot Bitcoin slipped in sympathy with the broader commodities rout, Twitter analysts and legacy financial talking heads immediately trotted out the old, exhausted playbook: Bitcoin’s war premium is dead. The narrative machine claimed that because the threat of regional escalation had cooled, the sole fundamental justification for holding a non-sovereign, hard-money asset had vanished. Mainstream models began predicting a cascading retreat back toward the $60,000 baseline, viewing Bitcoin as nothing more than an emotional barometer for global fear, an asset that thrives only when the world is burning.

The chart above shows that the removal of the energy-supply shock triggered a surge in semiconductor-heavy indicies like the Nikkei and oil-importing economies (Kopsi, Sensex)

They are completely misreading the plumbing.

Traditional analysts treat geopolitics like a psychological drama, measuring market impact through the fuzzy lens of investor sentiment. In reality, global macroeconomics is a mechanical system of pipes, valves, and dollar reserves. The legacy press looks at $82 oil and sees a world returning to a peaceful status quo, which they assume is inherently deflationary for a "safe-haven" asset like Bitcoin. They are blind to the underlying monetary reality. Peace at the Strait of Hormuz does not depress Bitcoin; it unburdens it. By removing the structural energy shock that has kept global central banks backed into a hawkish corner, this accord functions as a massive, hidden release valve for global fiat expansion. The $82 liquidity trigger isn't the end of a rally; it is the opening of the macroeconomic spigots.

Why Bitcoin's 34% War Rally Was a False Narrative

To understand why the 2026 peace accord is a structural catalyst for Bitcoin, we first have to dismantle the revisionist history surrounding the war itself. The talking heads spent the better part of the 106-day conflict pushing a tidy, romantic narrative: war breaks out, global tension spikes, and Bitcoin acts as the ultimate digital safe haven. It’s a compelling story for marketing brochures, but it’s completely disconnected from the actual data.

Geopolitical Chronology

The chronological reality of the conflict reveals a far messier picture. The match was lit on February 28, 2026, when U.S. and Israeli forces launched "Operation Epic Fury," a wave of preemptive strikes targeting Iranian nuclear infrastructure and command nodes. What followed was a masterclass in extreme diplomatic volatility. An April 7 ceasefire, brokered by Pakistani intermediaries, disintegrated in less than 24 hours following retaliatory rocket strikes on military installations in southern Lebanon. Days later, a high-stakes, face-to-face summit in Islamabad between U.S. Vice President JD Vance and Iranian parliamentary speaker Mohammad Bagher Ghalibaf completely collapsed over terms of regional containment. By April 13, Washington had formalised a strict naval blockade, choking maritime shipping and turning the Persian Gulf into a highly volatile geopolitical tinderbox.

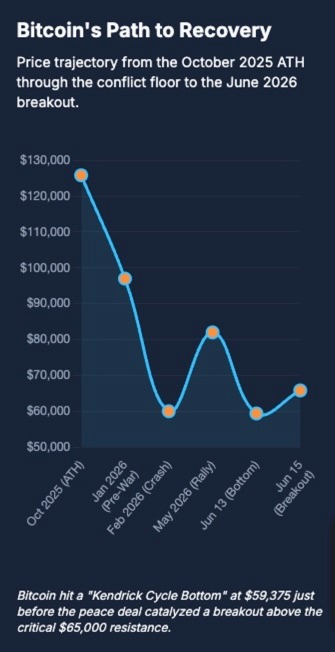

During the initial 12-day window of this rapid regional escalation, Bitcoin’s spot price notched a cumulative abnormal return of 34.1%. Academic papers were rushed to print, and commentators took victory laps on CNBC, celebrating this price spike as definitive proof that Bitcoin had finally cemented its status as "digital gold."

But if you look under the hood at the on-chain data, that narrative completely falls apart.

Exposing the Lie

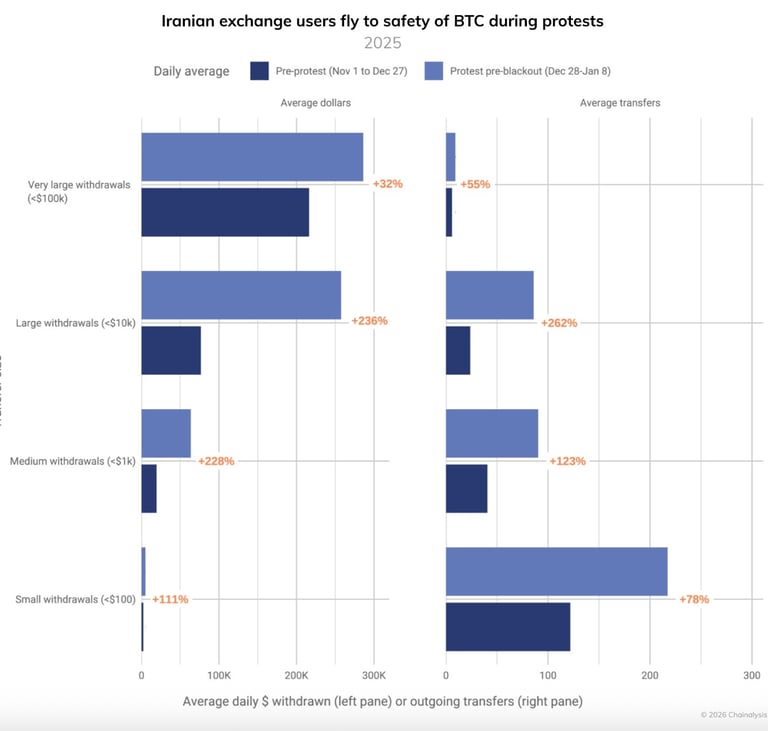

The initial 34.1% spike wasn't driven by a wave of sophisticated global capital seeking a flight to safety. It was a hyper-localized, frantic financial lifeline. On-chain volume showed a massive premium inside Iran and neighboring borders, driven entirely by citizens desperately dumping collapsing Iranian rials for any liquid, non-sovereign asset like gold and Bitcoin they could find before their banking access vanished. Beyond that frantic border panic, broader institutional price action across Western desks was brutally shackled.

The On-Chain Reality

To see what a real global flight to safety looks like, you only have to look at the physical gold market. Spot gold didn’t just rally; it surged to unprecedented record highs of $5,500 to $5,600 an ounce. This historic run was fueled by massive, non-sovereign central bank buying as foreign monetary authorities scrambled to de-dollarize their reserves out of fear of creeping Western sanctions. Bitcoin completely missed that institutional rotation.

The hard numbers prove that far from acting as a global safe haven, the war actually starved Bitcoin of the very Western institutional liquidity it needs to run. The chart above shows the performance of gold in blue, up a respectible 34% on a 1-year timeframe, while Bitcoin dropped 21%. During the conflict, the spot Bitcoin ETFs also suffered, experiencing a staggering $5.4 billion in cumulative net outflows. This included a record-breaking single-week exodus of $1.32 billion from BTC funds as risk-mitigation algorithms across Wall Street systematically liquidated speculative positions to hoard cash.

The market was so starved for oxygen by early June that it triggered what analysts called the "MicroStrategy effect." When a localized entity sold a tiny, insignificant fraction of 32 coins for $2.5 million, the order book was so thin that it sent an unhinged retail confidence shock wave through the market, causing a temporary flash crash. A truly deep, institutional safe-haven asset doesn't shudder when a tiny fraction of coins hits the tape. War didn’t validate Bitcoin’s risk-off thesis; it trapped the asset in a structural liquidity desert.

The Strait of Hormuz Paradox: How Peace Unburdens the Printing Presses

The mainstream financial press loves a simple correlation: high energy prices mean inflation, inflation means high interest rates, and high rates are bad for risky assets. But they miss the structural inversion that happens when a localized geopolitical shock turns into a systemic liquidity chokehold. The resolution of the 2026 energy crisis is not a story about cheaper oil; it is a story about the structural unburdening of global central bank printing presses.

The Macroeconomic Inversion

To understand why peace acts as an aggressive monetary accelerator, you have to look at the mechanical reality of the 2026 energy shock. When the formal naval blockade and retaliatory skirmishes effectively closed the Strait of Hormuz, they didn't just disrupt shipping routes; they forced devastating, friction-heavy maritime workarounds around the Cape of Good Hope. The mathematical consequence was immediate: Brent crude surged past $110 a barrel, and Murban crude cleared $100. This spike quickly bled into consumer psychology, forcing U.S. consumer inflation expectations to a three-year high of 4.2% in May, while Eurozone inflation ticked up to a stubborn 3.2%.

Central Banks in a Hawkish Corner

This energy-driven spike backed global central banks into a deeply defensive, hawkish corner. Monomaniacally focused on avoiding a 1970s-style wage-price spiral, monetary authorities had no choice but to sound aggressive. By late May, fixed-income markets were pricing in a suffocating 70% probability of an additional Federal Reserve interest rate hike. This looming threat of a prolonged "higher-for-longer" interest rate regime severely dried up global net liquidity. Institutional desks, squeezed by tightening financial conditions and falling equity markets, were forced to treat their highly liquid crypto positions as automated ATMs, liquidating their Bitcoin allocations to meet traditional equity margin calls and shore up corporate balance sheets.

The June 14 memorandum of understanding completely shatters this hawkish feedback loop.

Dismantling the Stagflation Threat

By unblocking the shipping channels on an immediate "toll-free" basis, the agreement instantly removes the structural logistics premium that was artificially bloating energy costs. As crude drops back toward baseline prices, the looming threat of stagflation, the absolute worst-case scenario for any monetary policy framework, simply evaporates.

This macro shift does two things. First, it immediately expands corporate operating margins by lowering input and transportation costs. Second, and more importantly, it gives central banks the exact macroeconomic cover they have been praying for. With the supply-side energy shock neutralized, inflation expectations will naturally cool. This allows central bank boards to abandon their aggressive defensive postures, quietly shelf any plans for further rate hikes, and begin laying the groundwork to open the global liquidity spigots once again. Bitcoin has spent months suffocating under a hawkish policy regime; peace just handed the central banks the oxygen tank.

The Net Liquidity Equation for the Rest of 2026

The Correlation Mirage

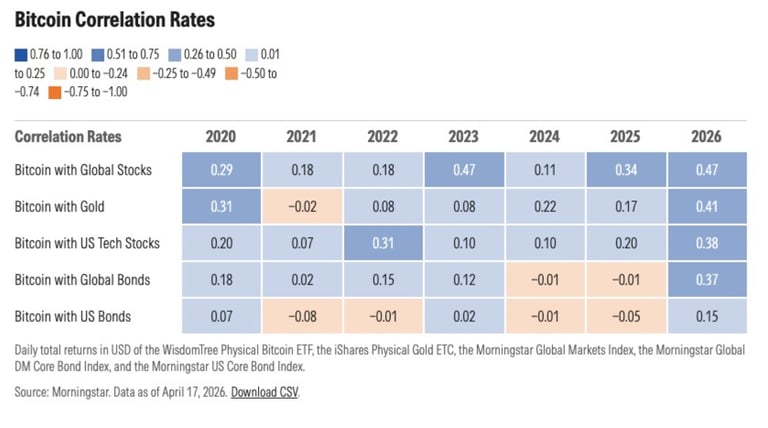

If you turn on any financial news network right now, you will hear a parade of macro strategists obsessing over Morningstar data that shows Bitcoin’s rolling correlation to the Nasdaq hovering at 0.5. They look at this number and confidently diagnose a "structural identity crisis," claiming that Bitcoin can't decide whether it wants to be an inflation hedge, a speculative tech stock, or a digital collector's item.

It is a completely superficial correlation mirage.

The True Target

Dismiss the narrative that Bitcoin is undergoing an existential dilemma. Bitcoin does not mimic tech stocks because investors are weighing its quarterly earnings reports or price-to-sales ratios against Apple or Nvidia. It correlates with the Nasdaq for a far simpler reason: both assets act as highly sensitive gauges for the sheer volume of fiat currency sloshing around the global financial architecture. Bitcoin isn't a tech stock; it is a pure mirror of global fiat expansion, tracking the global net liquidity index with a leveraged beta. When central banks tighten the screws, Bitcoin suffocates first; when they flood the pipes, Bitcoin absorbs the excess capital faster and more efficiently than any legacy asset on earth.

The Sovereignty Dividend

This is why the 2026 Global Peace Index's projected multi-trillion-dollar economic relief dividend is so critical for the rest of the year. That dividend isn't just an abstract statistic about saved defense spending; it is a mechanical calculation of capital that will filter directly back into global commercial banking reserves.

Consider the immediate structural pressure this peace deal removes from the global credit apparatus. Heading into the second half of 2026, highly indebted, energy-import dependent nations like Pakistan and Egypt were staring down a barrel. Facing brutal winter debt deadlines and an artificially inflated oil bill that drained their dollar reserves, these nations were on the absolute precipice of a systemic credit freeze. Had they defaulted under the weight of a $110 oil shock, the resulting contagion would have forced a massive contraction in global banking liquidity.

The newly eased global energy and credit environment completely alters that trajectory. With oil stabilized at $82, these sovereign balance sheets are thrown an immediate lifeline. International credit markets can unfreeze, cross-border capital flows can normalize, and global M2 can continue its upward expansion without the imminent threat of a sovereign default shock breaking the gears. By preventing a defensive, localized tightening of credit, this "sovereignty dividend" guarantees that the global liquidity river keeps flowing. For a pure liquidity sponge like Bitcoin, an expanding global M2 environment is the exact fuel required for its risk-on profile for a sustained Bitcoin bull run...Whenever that may actually happen, I fear taking a guess. More on that later.

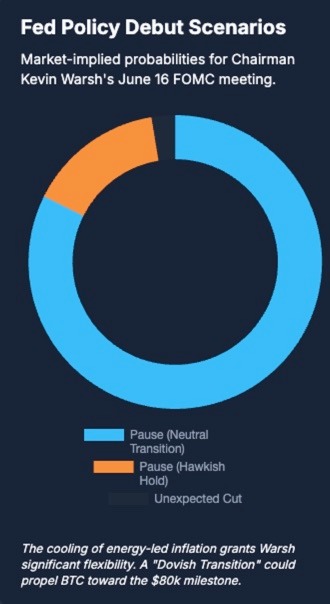

Monetary Policy Intersect: The Kevin Warsh FOMC Debut

Everything we know about central banking plumbing is about to hit an inflection point. June 16, 2026, marks the beginning of a two-day FOMC policy meeting that will fundamentally reshape the global macroeconomic landscape. This marks the debut of the newly appointed Federal Reserve Chairman, Kevin Warsh.

Sworn in on May 22, 2026, Warsh represents a stark, philosophical break from the Jerome Powell era. To understand the regime shift underway, you only have to look at his blunt Senate confirmation doctrine: "Inflation is a choice, and the Fed must take responsibility for it." No more hiding behind "transitory" supply chain excuses, and no more coddling Wall Street with over-communicated monetary policy. Warsh views the Fed’s primary mandate through an aggressive, structural lens. His arrival introduces a completely new set of rules for global capital markets, the Warsh Doctrine, which is built upon four foundational pillars.

The Four Pillars of the Warsh Doctrine

Skepticism of Forward Guidance: Warsh intends to dismantle the quarterly "dot plot" regime, viewing rigid, long-term interest rate projections as a trap that limits the Fed's flexibility and creates artificial market entitlement. Instead, he favors a return to Alan Greenspan’s philosophy of "strategic ambiguity", forcing trading desks to react to real-time economic data rather than hand-fed policy promises.

Balance Sheet Reduction over Benchmark Rates: This is the big one for structural liquidity. The core of the Warsh Doctrine is an aggressive acceleration of Quantitative Tightening (QT). He believes a bloated central bank balance sheet distorts asset prices and misallocates capital. Warsh prefers to aggressively shrink the Fed’s bond portfolio while simultaneously keeping benchmark interest rates low enough to support everyday households and businesses.

The AI Disinflationary Thesis: Unlike legacy economists who view inflation purely through demand-side models, Warsh integrates real-world technological shifts. He argues that technology-driven productivity gains, specifically the mass deployment of enterprise AI workflows, naturally apply structural downward pressure on prices, inherently lowering the long-term equilibrium interest rate.

Trimmed-Mean Metrics: Warsh has publicly stated that he will focus less on headline Personal Consumption Expenditures (PCE) or Consumer Price Index (CPI) numbers that get whipped around by short-term supply chain anomalies. Under his leadership, the Fed will judge underlying inflationary realities strictly through trimmed-mean metrics, cutting out the volatile statistical noise at both tails of the distribution.

The Post-Peace Scenarios: A Fork in the Road

With the federal funds rate currently held at 3.50% to 3.75%, the timing of the June 14 peace accord presents the new Chairman with an extraordinary macro backdrop for his debut. The immediate collapse of oil prices gives Warsh a powerful tactical tool. However, because his doctrine values data over narrative, the macro landscape now splits into two distinct paths for global capital flows.

Scenario A: The Dovish / Neutral Transition (The Liquidity Pump)

In this scenario, the mechanical reality of $82 oil flows directly into the Fed’s models, pulling intermediate inflation expectations sharply back down toward the 2.0% target. This swift reversal gives Warsh the exact macroeconomic cover he needs to implement his ideal policy mix.

The Fed can comfortably preserve or even accelerate its projected late-2026 interest rate cuts to ease the burden on commercial banking channels. Because the Fed is simultaneously letting long-duration bonds roll off its balance sheet while lowering short-term rates, the yield curve will steepen dramatically. This structural steepening acts as an absolute green light for institutional risk-taking.

Concurrently, the U.S. Dollar Index (DXY) will retreat decisively from its recent peak of 97.6 as the global dash for cash subsides. For Bitcoin, this is the ultimate macro cocktail. As the dollar softens and real yields ease, a tidal wave of unburdened Western institutional capital will flow directly into global liquidity sponges, giving Bitcoin the precise monetary fuel it needs to blast through overhead resistance.

Scenario B: The Hawkish / Higher-for-Longer (The Capital Flight)

The cynical alternative rests on structural inertia. Even with oil plunging to $82, Warsh's reliance on trimmed-mean metrics could work against short-term market bulls. If the incoming data shows that core services inflation remains sticky and year-end PCE projections are revised upward due to the lag in housing and labor markets, the Warsh Doctrine will show its teeth.

True to his word that "inflation is a choice," Warsh could completely erase any remaining rate cuts for the rest of 2026, digging his heels into a prolonged, defensive "higher-for-longer" stance. In this environment, the market’s initial peace euphoria will evaporate.

The DXY will pick up its upward trajectory, draining liquidity from global markets as international banks scramble to defend their currencies. Speculative and institutional capital will instantly flee high-beta assets to hide out in yielding cash instruments, forcing Bitcoin back down to retest major horizontal support floors. Warsh's debut has turned this week's FOMC meeting into an absolute binary junction for Bitcoin's risk profile.

Crucial Fragilities and Geopolitical Spoilers to the Peace Accord

Everyone who studies finance knows that markets hate uncertainty, but they absolutely despise a false sense of security. Right now, the financial world is pricing in the June 14 memorandum of understanding as if it were a done deal, painting a clean, frictionless picture of global stability.

That is a dangerous, rookie mistake.

As any veteran of geopolitical risk knows, there is a massive, volatile gap between a preliminary piece of paper signed by diplomats and a permanent, legally binding peace treaty. With the official signing summit scheduled for Friday, June 19, 2026, in Geneva, we are entering a four-day execution window littered with systemic landmines. If you are managing capital, you cannot look at this accord with rose-colored glasses. You have to analyze the execution risk delta, and right now, there are three fatal points of failure that could instantly rip this agreement to shreds and send market volatility into orbit.

The Three Fatal Points of Failure:

1. The Israel-Lebanon Detachment

The ink wasn't even dry on the Tehran announcement when the fragile illusion of regional peace shattered. Early June 15, the Israeli Air Force launched a series of heavy airstrikes targeting tactical positions across Beirut. Prime Minister Benjamin Netanyahu wasted no time drawing a line in the sand, explicitly declaring that Israel is not a party to the U.S.-Iran agreement and will not be bound by Washington’s diplomatic timelines.

This creates an immediate, highly combustible decoupling. Even if Washington and Tehran want to de-escalate, Iran’s proxy network retains full operational autonomy. A single, high-casualty retaliatory strike by Hezbollah into northern Israel would trigger an instantaneous, uncontainable escalation chain. Netanyahu’s kinetic actions prove that the core regional conflict remains completely detached from the U.S. diplomatic track. If the proxies strike back, the broader ceasefire collapses before the diplomats can even pack their bags for Geneva.

2. Unresolved Nuclear Terms and Asset Releases

The second landmine is the sheer financial and political friction surrounding the proposed economic terms. The framework dictates an initial unfreezing of $12.5 billion out of a total $25 billion in restricted Iranian assets as a gesture of good faith. The domestic political blowback on both sides was immediate and fierce.

The reality on the ground in Tehran is just as hostile. The ultrahardline Paydari (Stability) Front has already mobilized massive street protests, screaming that the Rouhani-led diplomatic team sold out Iran's sovereign nuclear achievements for pennies on the dollar. The leadership in both capitals is operating in a domestic political pressure cooker; if either side blinks or alters the asset schedule to appease their domestic base, the entire treaty structure defaults.

3. The Strait of Hormuz Operational Control

The final, and most structurally critical, point of failure lies in the literal plumbing of the global energy supply. The White House has been triumphantly trumpeting a "toll-free," open maritime channel. However, reports directly from Iran’s state-aligned Mehr news agency present a completely different reality, stating that the memorandum permits the reopening of the Strait exclusively under "Iranian maritime arrangements" within a loose 30-day window.

U.S. naval authorities in the region have already called that interpretation completely unacceptable, refusing to cede operational control or accept arbitrary screening protocols from the Islamic Revolutionary Guard Corps (IRGC). Compounding this operational friction is a brutal physical reality. As Landon Derentz from the Atlantic Council recently warned, even if both sides agree on the paperwork, the actual return of energy infrastructure will be a long, grinding process. The strait is still littered with active naval minefields, and damaged offshore loading facilities mean that physical oil flows cannot simply be switched back on overnight. The market has priced in an immediate supply restoration, but the operational reality suggests a slow, friction-heavy transition prone to accidental military triggers.

The Post-Conflict Arbitrage Facing Institutional Capital

All of this tension, macro positioning, and geopolitical posturing culminates in a massive, glaring market inefficiency. As of today, June 16, 2026, we are looking at a generational mispricing across the digital asset landscape.

The Generational Mispricing

While the legacy trading desks are busy panicking over the execution details of the peace accord, the market's microstructure has quietly pulled off a massive technical breakout. Bitcoin has cleared its heavy horizontal resistance at $64,000, shown in green, and is trading firmly at $65,794. In its wake, Ethereum has reclaimed the critical $1,731 level, and XRP is flashing a stark MACD buy signal above $1.18.

Yet, despite this structural shift, the institutional capital allocators are completely paralyzed. Spot ETF inflows are scraping multi-month lows, and the Crypto Fear and Greed Index is trapped in "Extreme Fear" at a reading of 20, painfully crawling out from an absolute cyclical bottom of 8. The institutional herd is so skeptical, resulting from the recent headlines, that it will take some time before faith and confidence is regained.

The Overhead Battlegrounds

The technical reality on the ground, mapped out by analysts at Bloomberg, states that this is likely going to be a local bounce, not a bottom for Bitcoin, as structural frailties in the asset are exposed.

While there is sentiment from other analysts stating that Bitcoin is currently consolidating above its 4-hour 20-period and 50-period Exponential Moving Averages (EMAs), which have clustered into a supportive cushion in the $63,600 to $63,700 range. At the same time, the Average True Range (ATR) is compressing near 890, signaling that this quiet, sideways grind is the prelude to an explosive volatility expansion. But it is important to note that Bitcoin's price failed to close above the 100-day EMA, which is now acting as resistance, meaning I am inclined to disagree with the sentiment that this is the beginning of a major leg up. Bitcoin has a lot of work to do before it regains the confidence of global investors to start injecting liquidity back into the asset.

While industry analysts struggle to make heads or tails of this crypto market in the short term, the real war will be fought at the critical structural boundary between the $74,000 and $75,000 price bands. This zone marks the exact 0.618 Fibonacci retracement of the 2025 all-time high bearish impulse, heavily reinforced by the descending 200-day EMA.

The playbook here is entirely binary. A volume-backed, daily close above $75,000 utterly destroys the macro downtrend, shifting the market paradigm from defensive accumulation to an aggressive, parabolic expansion. Conversely, if the execution risks we analyzed earlier catch up to us and the $59,000 horizontal floor breaks, expect risk engines to dump, triggering a rapid, cascading capitulation down to the deep $52,000 institutional demand zone.

For me personally, I am ignoring the noise of all the data points and all the talking heads and sticking to a tried and true method of price analysis. In my nearly 10 years in this industry, I have never heard so many contradictory stances regarding price. If we look at previous cycles, analysts such as Benjamin Cowan and Dan Krupka paint a bearish picture for the remainder of the year. Bitwise CIO Matt Hogan, Analyst Jordi Visser, the likes of Anthony Pompliano, Kathy Wood of Arc Invest, and others are bullish for the end of the year. So...Toss a coin? It is a tug of war, and time will tell who is correct.

For me, this time around is easy. I will be keeping an eye on interest rates, M2 money supply (looking for QE), geopolitical tensions, and watching the 200-day moving average on the daily chart, and won't be deploying much capital until Bitcoin's price can confidently close above that to signal a confirmed bull market. I've caught enough falling knives in my day to want to avoid too many more.

The Institutional Bridge Is Already Built

What makes the current institutional paralysis so deeply ironic, and makes it even more difficult to map out for investors, is that the operational bridges connecting Wall Street to this asset class have never been sturdier, creating a complete disconnect between fundamentals and price. While traders hesitate, the structural plumbing continues to lock into place behind the scenes:

The ETF Evolution: The SEC has quietly granted approval for NYSE Arca to list and trade T. Rowe Price’s new actively managed crypto ETF, signaling a major transition from simple spot trackers to sophisticated, yield-generating Wall Street vehicles.

Public Equities Integration: Bitmine’s preferred shares (ticker: BMNP) have officially listed on the New York Stock Exchange, capturing massive institutional eyeballs by offering a structured 9.50% dividend backed entirely by digital asset infrastructure.

Regulatory De-risking: The CFTC has issued a pivotal No-Action letter regarding perpetual digital commodity contracts, effectively giving institutional derivative desks the legal green light to clear high-volume crypto swaps without structural fear of regulatory reprisal.

The Final Strike

Yet, Wall Street sits frozen, pointing to domestic political gridlock, like the highly anticipated, inevitable failure of Congress to pass the CLARITY Act before the upcoming July 4 recess, as an excuse to stay in cash. They are completely missing the forest for the trees.

The political theater in Washington is a sideshow. The mechanical reality of the U.S.-Iran peace deal has structurally cleared the runway, neutralized the threat of a stagflationary spiral, and primed the ultimate global liquidity accelerator. It's just a matter of when, not if.

So the ultimate question falls squarely on the institutional allocators: Will Wall Street wake up and realize they are looking at a fundamentally de-risked asset class priced at a steep geopolitical discount? Or will they freeze in fear, trapped in their legacy frameworks, until the central bank printing presses inevitably force them to buy back their allocations at the absolute all-time highs?

Tayler McCracken- Crypto Analyst

Tayler McCracken is a veteran crypto journalist and media executive with nearly a decade of experience directing editorial strategies for the sector's largest outlets—including roles as Editor-in-Chief at Coin Bureau and Head of Content for 99Bitcoins. Combining a background in traditional banking with studies in computer information systems, his market insights have anchored coverage across Nasdaq, Yahoo Finance, and MSN News.

Image Source: Chainalysis