June 22-26 Market Brief: Liquidity Repricing and Value-Capture Leakage

Markets are recalibrating as Fed Chair Kevin Warsh delivers a hawkish regime shift. While US M2 supply expands to $23.05 trillion, the crypto ecosystem is preparing for the massive "Glamsterdam" upgrade amidst persistent institutional ETF outflows.

WEEKLY MARKET BRIEFS

Tayler McCracken

6/16/202613 min read

Executive Summary

A structural hawkish shift by the Federal Open Market Committee under newly appointed Chair Kevin Warsh, which held rates at 3.50% to 3.75% but revised the median 2026 dot plot upward to 3.8% and elevated the Q4 core PCE inflation projection to 3.3%, triggered an aggressive institutional de-risking wave that flushed over $122 million in leveraged longs within a 24-hour window. This macroeconomic tightening forced Bitcoin to slide from its weekly high down to $62,242 before stabilizing near $62,644, while Ethereum capitulated to $1,671.31, underperforming due to severe mainnet value-capture degradation, where Layer-2 networks retained a staggering 99.58% of fee revenues. Concurrently, US spot Bitcoin ETFs bled -$226.84 million in net weekly outflows as allocators rotated capital into high-beta artificial intelligence equities, though the downside was partially absorbed by corporate treasury accumulation as Strategy acquired 520 BTC, expanding its total balance sheet to 847,363 BTC.

Tayler McCracken- Crypto Analyst

Tayler McCracken is a veteran crypto journalist and media executive with nearly a decade of experience directing editorial strategies for the sector's largest outlets—including roles as Editor-in-Chief at Coin Bureau and Head of Content for 99Bitcoins. Combining a background in traditional banking with studies in computer information systems, his market insights have anchored coverage across Nasdaq, Yahoo Finance, and MSN News.

Key Takeaways

Monetary Reality Check: The upward revision of the median dot plot to 3.8% and the core PCE projection to 3.3% explicitly kills the "rate cut summer" narrative, signaling entrenched structural inflation that will subject risk assets to restrictive macro headwinds for the next 2–4 weeks.- This is a bearish development for risk-on asset holders holding their breath for a rate cut.

The Sovereign Gravity Well: The 10-year US Treasury yield surging to 4.51% acts as a powerful gravity well for speculative capital, shifting institutional allocations away from digital assets into high-performing AI equities, despite an expansionary M2 money supply ($23.05 trillion) providing long-term structural tailwinds.- This is a bearish development as it will be redirecting capital away from digital assets.

Ethereum's Economic Leakage: The widening L2 value-capture gap, where top execution networks generated $10.02 million in fees but returned a pathetic 0.42% rent to the L1 base layer, exposes ETH as an inefficient monetary asset ahead of the "Glamsterdam" upgrade, ensuring near-term underperformance relative to BTC.- This inefficiency in ETH as a base asset is not great for Ethereum holders.

Flight to Self-Custody and Quality: High-volume exchange net outflows, including a16z extracting 25,560 ETH from Binance, reveal deep long-term institutional conviction, driving capital out of speculative, high-FDV L1 assets into functional DeFi protocols and resilient ecosystems holding critical technical moving averages.- This is a positive catalyst for digital asset holders as it shows institutional flows and retail flows into long-term storage on assets they are bullish on.

Legislative Defense Moats: The Senate's bipartisan passage of the CBDC prohibition within the 21st Century ROAD to Housing Act marks a historic structural win for self-custody and privacy rights, running parallel to the CLARITY Act's advancement toward a full Senate floor vote.- This is a major positive catalyst not just for crypto, but for the ethics and ethos of privacy and self-custody that Bitcoin was founded upon.

Macro & Market Structure

The Liquidity Regime

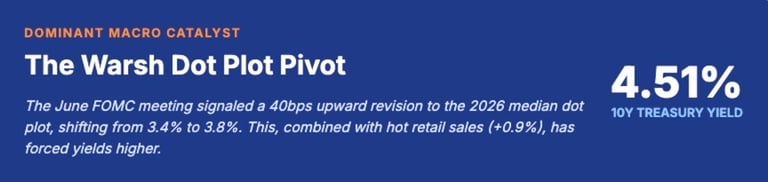

Global liquidity is navigating a highly restrictive monetary regime characterized by stubborn inflation and central bank divergence. The domestic broad money supply (M2) expanded to $23.05 trillion in May 2026, marking a 1.09% month-over-month and 5.58% year-over-year growth trajectory. However, this systemic liquidity expansion faces an aggressive headwind from the Federal Reserve's hawkish policy shift under Kevin Warsh, where the median dot plot climbed to 3.8% and the Q4 core PCE forecast was jacked up to 3.3%.

Concurrently, the Fed altered its money stock netting methodology, shifting to aggregate netting for IRA and Keogh balances from retail money market funds, inflating component lines on paper while leaving net non-seasonally adjusted totals unchanged. On the sovereign front, the 10-year US Treasury yield spiked violently to 4.51% following hot May retail sales (+0.9%), establishing a high risk-free rate environment that pressures long-duration risk assets. Globally, the European Central Bank's aggressive 25 basis point hike on June 11 contrasts sharply with the Swiss National Bank's decision to freeze its policy rate at 0%, revealing an asymmetrical macro tightening environment ahead of the crucial May PCE print.

My Take

The market is panicking over Kevin Warsh’s hawkish dot-plot pivot and the violent spike in the 10-year Treasury yield to 4.51%, but they are entirely missing the fact that underlying liquidity mechanics under a structurally expanding M2 money supply, now sitting at $23.05 trillion and growing at a 5.58% year-over-year clip, haven't actually choked off the system.

The Netting Illusion: The Fed’s accounting tweak for IRA and Keogh balances is pure noise. It inflates retail money market component lines on paper, giving a false impression of organic expansion where net unadjusted totals remain completely unchanged.

Asymmetrical Fractures: The global monetary front is completely decentralized. The ECB's aggressive hike contrasted against the SNB's freeze proves that global tightening is no longer a synchronized march. Capital will naturally seek out the high risk-free rate environment of the US, paradoxically buffering domestic dollar liquidity.

The Move: Stop treating this yield spike as a permanent structural shift in the cost of capital. It is an impulsive macro reaction to a hot retail print and a changing of the guard at the Fed. The absolute volume of dollars in the system is rising despite the hawkish rhetoric. I'm holding steady on long-duration allocations through the upcoming May PCE print; the headline panic is masking a secular liquidity floor.

Asset Performance & Correlations

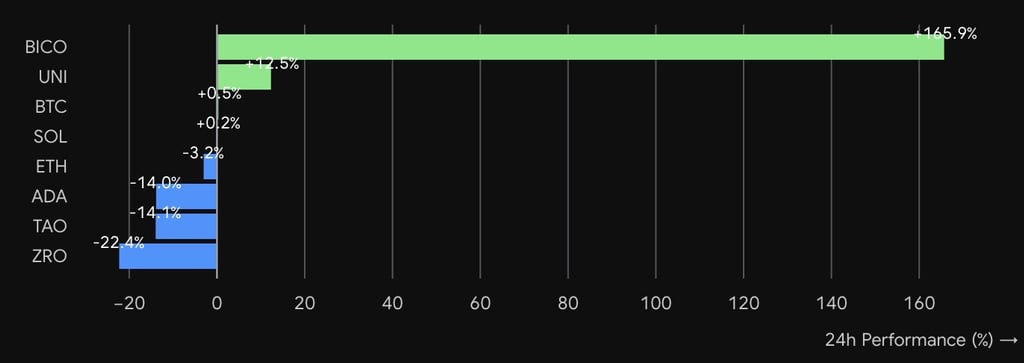

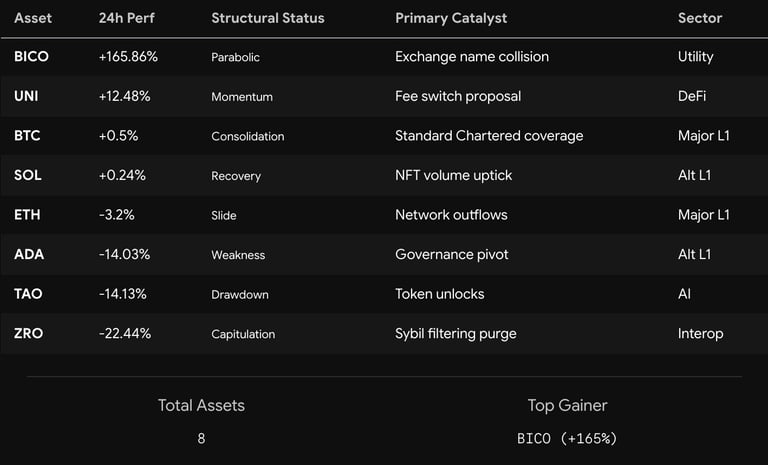

The crypto market is currently operating in a highly fragmented, idiosyncratic regime. While majors like BTC and ETH chop sideways in tight ranges, massive alpha or capitulation is being driven entirely by micro-catalysts, ranging from structural unlocks (ZRO) to institutional validation (UNI) and bizarre retail mix-ups (BICO).

Market Structure Breakdown

The Volatility Anomalies: BICO's massive +165.86% surge is an extreme outlier driven purely by reflexivity and technical confusion (ticker collision), while ZRO represents a textbook structural supply overhang with its 25.71M token unlock dragging it down over 22%.

Decoupled DeFi: UNI is showing strong counter-cyclical strength (+12.48%), proving that top-tier DeFi protocols can separate from the macro layer-1 drag when handed explicit institutional tailwinds like Standard Chartered's coverage.

The L1 Rotation Drag: Old-guard alternative L1s like ADA are bleeding out to multi-year lows (-14.03%), and newer narrative plays like TAO are suffering from broader tech equity de-risking, while SOL barely holds its ground at the 21 EMA.

Digital asset spot markets exhibited synchronized downside correlation with traditional risk assets, driven entirely by the hawkish repricing of the US sovereign yield curve. As the 10-year Treasury yield surged to 4.51%, it initiated an aggressive rotation out of digital assets and precious metals like gold. Allocators aggressively diverted capital into high-performing artificial intelligence equities as Bitcoin's risk-on profile comes under question, treating legacy tech as a preferred growth vehicle over digital assets. This rotation inflicted uniform damage across high-FDV alternative Layer-1 networks, causing assets like TAO and ADA to contract sharply by over 14%.

Conversely, the week exposed sharp correlation inversions within the crypto complex itself. While major capitalization indices fell uniformly, the CF DeFi Composite Index restricted its weekly decline to just -1.14%, detaching completely from the broader down-leg. This internal divergence highlights a structural rotation away from speculative alternative L1 infrastructure and toward functional utility, on-chain fee generation, and battle-tested cash-flow protocols like Uniswap, which posted a counter-cyclical +12.48% rally.

My Take:

This is a positive pivot in the crypto markets as we see capital flying back into genuine protocols and productive decentralized applications. This is a sign of maturation after the flight of speculative capital into meme coins and AI projects with no future or intentions of follow-through.

Technicals: The Majors

Bitcoin: Liquidity Exhaustion Corporate Backstop

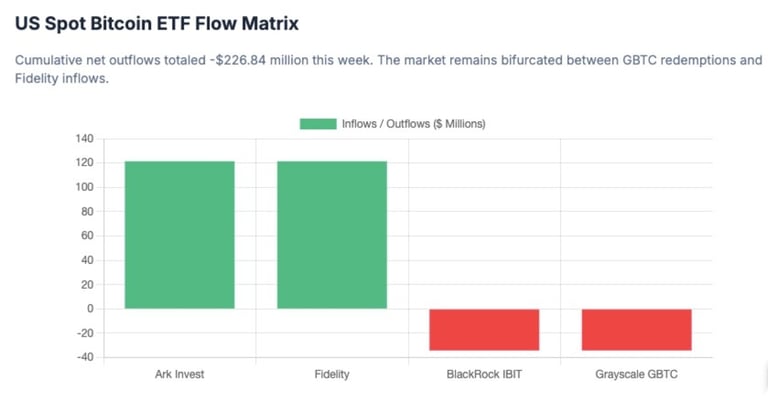

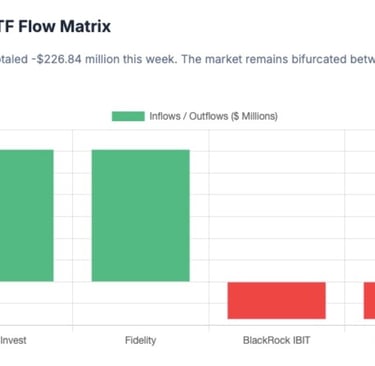

Bitcoin entered a strict consolidation phase between $62,000 and $64,824, demonstrating a pronounced contraction in daily spot volume that signals an equilibrium of buyer and seller exhaustion. Regulated US spot Bitcoin ETFs experienced net weekly outflows of -$226.84 million, highlighted by intense daily redemptions of $68.18 million from BlackRock's IBIT and Grayscale's GBTC on June 22.

This institutional de-risking forced a leverage flush, absorbing over $122 million in long liquidations before a volatile positioning reset triggered a short squeeze generating $112 million in short capitulations. Crucially, corporate treasury demand acts as the primary economic backstop to this ETF-led distribution; Strategy exploited the correction to acquire 520 BTC at an average price of $67,068 between June 15 and June 21, elevating its total treasury allocation to 847,363 BTC at an aggregate cost basis of $75,651 per coin. This relentless corporate accumulation absorbs spot supply, pointing to a hollowing out of exchange float as retail sellers capitulate to long-term holders.

My Take:

This is a mixed bag, as ETF outflows of this magnitude are never a good look for the digital asset space. It shows an unfortunate lack of trust and confidence in the asset. However, outflows of this magnitude is also a likely sign that we are closer to the bottom of this cycle and Bitcoin is closer to finding its floor.

Ethereum: L2 Value Capture Leakage

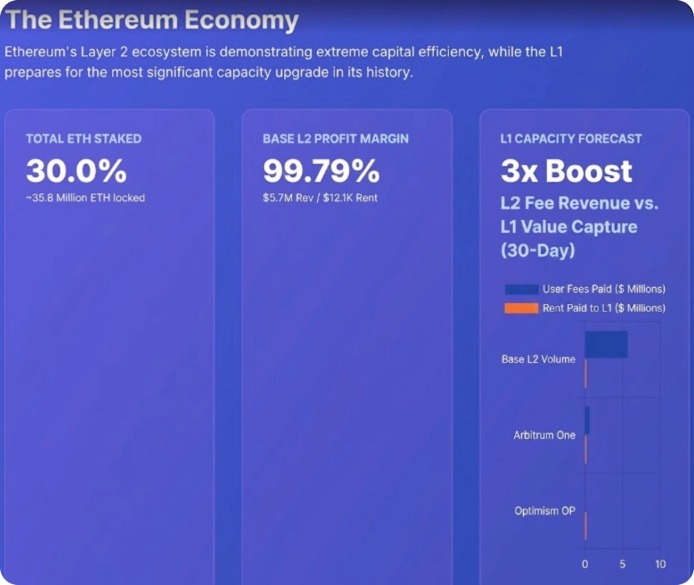

Ethereum faces severe structural price decay, sliding from an opening print of $1,732.82 to close at $1,671.31, an underperformance driven directly by the L2 value-capture gap. Over a rolling 30-day window ending June 9, 2026, top Layer-2 execution networks generated $10.02 million in aggregate user transaction fees but returned a minor $42,000 in settlement rent to the Ethereum L1 base layer, a nominal 0.42% value-capture rate that strips mainnet stakers of fee-burn mechanics. Base captured 36.7% of daily L2 transaction share (9.92 million daily transactions) to generate $5.72 million in fees while paying just $12.1K in L1 rent, pocketing a 99.79% profit margin. This economic imbalance positions ETH more as a pure technology platform than an efficient monetary asset, keeping the native token depressed. However, the network's consensus security layer remains fundamentally anchored by a record staking milestone; approximately 30% of the circulating supply (~35.8 million ETH) is locked in staking contracts, providing a 3.5% to 4.5% non-inflationary yield environment that limits structural downside and positions the asset for a violent upward squeeze once macro interest returns.

My Take:

The market is panicking over Ethereum’s severe structural price decay and its slide from $1,732.82 to $1,671.31, but they are entirely missing the fact that while protocol value is actively leaking to Layer-2 execution environments, the native asset's underlying supply mechanics are winding up a massive coiled spring.

The Parasitic L2 Racket: Layer-2 networks have effectively decoupled scaling from L1 value accrual. Base pocketing a 99.79% profit margin, generating $5.72 million in user fees while paying a measly $12.1K in L1 rent, proves that the tiny 0.42% aggregate value-capture rate has completely gutted mainnet fee-burn mechanics. ETH is currently priced as a cheap infrastructure settlement layer rather than an efficient monetary asset.

The Illiquidity Floor: Despite the brutal fee-capture metrics, the consensus layer is fundamentally anchored. Locking up roughly 30% of the circulating supply (~35.8 million ETH) creates an immense structural supply sink. Stakers are happily swallowing a 3.5% to 4.5% non-inflationary yield, completely removing that asset base from the liquid sell-side market.

In my opinion, seeing a collapse in mainnet fee generation as a permanent valuation death spiral is the wrong way to look at it. The metric is depressed because the technical architecture shifted to cheap blob data, but the asset's structural floor is rock solid. Treat this L2 value-capture gap as a long-term accumulation window. The massive supply bottleneck created by record staking ensures that the moment macro interest shifts back to crypto, the sheer lack of liquid mainnet supply will trigger a violent upward squeeze.

Sector Spotlight: Decentralized Finance Resilience

While broader crypto assets capitulated under macro pressure, the decentralized finance (DeFi) sector demonstrated strong structural resilience, serving as a haven for capital hunting functional utility over speculative alternative assets. The counter-cyclical rotation was validated on June 15 when Standard Chartered initiated institutional research coverage on Uniswap (UNI), driving a +12.48% breakout by legitimizing automated market maker economies and on-chain fee structures.

This sector-wide flight to quality is reinforced by significant whale movements; venture capital titan Andreessen Horowitz (a16z) executed a massive risk-mitigation move on June 23, withdrawing 25,560 ETH (~$43 million) from Binance to institutional self-custody wallets, compounding a broader June trend that saw 475,000 ETH completely removed from centralized exchange order books.

Conversely, interoperability and decentralized AI sectors faced severe liquidation, with LayerZero (ZRO) plunging -22.44% due to the structural supply shock of a 25.71 million token unlock ($23 million value), and Bittensor (TAO) shedding -14.13% via aggressive profit-taking. The long-term viability of high-revenue DeFi protocols and robust ecosystems like Solana, which closed green at +0.24% while holding its daily 21 EMA and absorbing $3 million in ETP inflows, is fundamentally superior to high-FDV alternative Layer-1 networks. Capital is permanently fleeing ecosystems lacking organic cash flow, making functional DeFi a high-conviction medium-term play while alternative L1s face terminal dilution.

My Take:

I see this trend as overall net positive as anyone serious in the crypto space would tell you we would love to see another "DeFi Summer" instance, where the speculative capital is flushed out of all the non-productive (garbage) crypto projects and return to DeFi products that move our space forward, returning this industry on its original trajectory of democratizing finance and creating a better financial system that is non-permissioned and immutable.

On-Chain Intelligence

On-chain capital footprints reveal an intense bifurcation between smart money long-term accumulation and retail panic. The withdrawal of 475,000 ETH from centralized exchanges to cold storage throughout June indicates a massive institutional flight to self-custody, signaling that sophisticated market participants view the current price compression as a strategic accumulation zone rather than a structural trend reversal. This thesis is verified by a16z's $43 million extraction of 25,560 ETH from Binance to secure native validator yields. While exchange net flows and whale wallet movements confirm institutional accumulation, stablecoin velocity metrics remain unverified across primary networks.

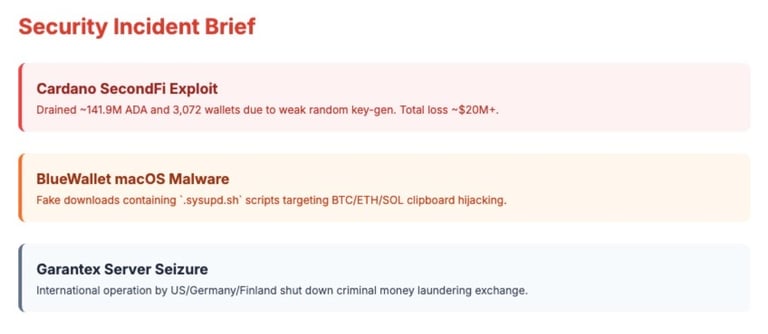

Conversely, retail capitulation was heavily concentrated in the alternative L1 sector following the SecondFi wallet exploit in the Cardano ecosystem on June 21, which mathematically derived private keys via weak randomness. This client-side vulnerability triggered two distinct waves compromising 3,072 unique wallets and draining 141.9 million ADA. While SecondFi successfully isolated 129 million ADA in a secure vault address (addr1qxd39k4…wxpl3), the remaining ~12 million ADA was immediately flushed through the Minswap DEX pool, driving native ADA down over 13% to five-year lows of $0.147 as retail panic-sold into a localized liquidity vacuum.

Regulatory & Policy Watch

The legislative architecture of the United States digital asset market is rapidly consolidating, drawing permanent jurisdictional boundaries that establish distinct compliance moats for regulated entities. The Senate Banking Committee's 15-9 bipartisan passage of the Digital Asset Market CLARITY Act (H.R. 3633) on May 14, and its subsequent placement on the Senate Legislative Calendar under General Orders (Calendar No. 423) on June 1, positions the bill for a critical floor vote. The House of Representatives has synchronized its momentum, scheduling a high-impact New York hearing for July 17, 2026. The CLARITY Act permanently codifies the CFTC's exclusive oversight over "digital commodities", explicitly naming Bitcoin, Ethereum, and XRP, while restricting the SEC to traditional securities mandates. This framework permanently alters industry economics by forcing centralized exchanges to register with the CFTC, segregate customer funds, and adhere strictly to Bank Secrecy Act AML protocols.

Simultaneously, anti-CBDC sentiment achieved a massive legislative victory as the Senate passed the 21st Century ROAD to Housing Act in an 85-5 vote on June 22, appending a binding provision that explicitly prohibits the Federal Reserve from issuing a central bank digital currency directly or indirectly through December 31, 2030. Internationally, the Bank of England established a strict £40 billion stablecoin issuer cap while removing individual holding limits to fast-track commercial payment integration, expanding compliance moats for capitalized players while state law enforcement aggressively eliminated non-compliant actors via the tri-jurisdictional server seizure of the money-laundering exchange Garantex on June 23.

My Take

The market is looking at this sudden rush of legislative activity as a wave of restrictive regulatory tightening, but the rapid consolidation around the CLARITY Act and anti-CBDC provisions could be a massive structural forcing function building permanent compliance moats for heavily capitalized, compliant monopolies.

The SEC Castration: Permanently codifying the CFTC’s exclusive oversight over Bitcoin, Ethereum, and XRP effectively strips the SEC of its aggressive "regulation-by-enforcement" mandate. This delivers the exact legal finality institutional allocators need to aggressively deploy capital without fear of retroactive litigation.

The Stablecoin Protected Monopoly: Appending a hard statutory ban on a Federal Reserve retail CBDC through 2030 inside the bipartisan housing package is a complete capitulation by the state. Washington has officially abdicated the sovereign digital dollar space to the private sector for the next five years. This secures a massive, protected runway for hyper-compliant private stablecoin issuers and yield-bearing Real-World Assets (RWAs).

The Global Liquidity Sterilization: The Bank of England’s strict £40 billion issuer cap and the coordinated tri-jurisdictional takedown of Garantex show the regulatory perimeter being weaponized in real time. The state is systematically suffocating grey-market, non-compliant offshore rails not to destroy the asset class, but to clear the playing field exclusively for banking and payment incumbents.

This is a deliberate, state-sanctioned transition from a retail-driven wild west to an institutional playground. I have been and will continue to deploy capital within the statutory safe havens explicitly carved out by this legislation, specifically major L1 digital commodities (BTC, ETH,) and compliant, institutional stablecoin/RWA infrastructure. The wild-west alpha is dead, but the institutional moat alpha is just beginning to scale.

Upcoming Events to Watch

May PCE Price Index Release (Thursday, June 25, 2026): The Federal Reserve's primary inflation gauge is expected to print at 3.3% to 3.4% year-over-year for the core metric. Market liquidity will aggressively front-run this data; any upside deviation will immediately solidify Kevin Warsh's hawkish policy trajectory, driving a secondary leg down in risk assets and pushing sovereign yields higher.

Deribit Monthly Options Expiry (Friday, June 26, 2026 - 08:00 UTC): A massive derivatives settlement event that will introduce intense localized volatility. Market makers will be forced to aggressively re-hedge and adjust gamma positioning around core option strikes, driving choppy spot price action immediately preceding the settlement.

June Consumer Confidence Index (Tuesday, June 30, 2026): Serves as a vital macro signal for underlying household spending power, directly impacting broader equity market momentum and digital asset capital inflows.

MiCA Full Compliance Deadline (Wednesday, July 1, 2026): This marks the formal end of the transitional window for stablecoin issuers and Crypto-Asset Service Providers (CASPs) in the European Union. Non-compliant platforms face immediate trading pair suspensions, causing localized liquidity friction across EUR-denominated markets while compliant entities (such as Ripple via its Luxembourg approval) secure dominant market shares.

June Non-Farm Payrolls (NFP) Release (Thursday, July 2, 2026): Shipped one day early due to the federal holiday weekend, this employment print serves as the final critical labor-market input for the Federal Reserve's July 28–29 FOMC meeting, directly dictating near-term global dollar liquidity.

FOMC Minutes Release (Wednesday, July 8, 2026): Detailed internal disclosures regarding the committee's hawkish policy shift will release, allowing macro desks to price in the exact probability of an upcoming terminal rate hike.